Key Takeaways

- Fintech app development cost starts around in the tens of thousands for a narrow MVP and rises to $1M+ for enterprise-grade products as compliance, integrations, and security scope expand.

- In this guide, typical MVP budgets include:

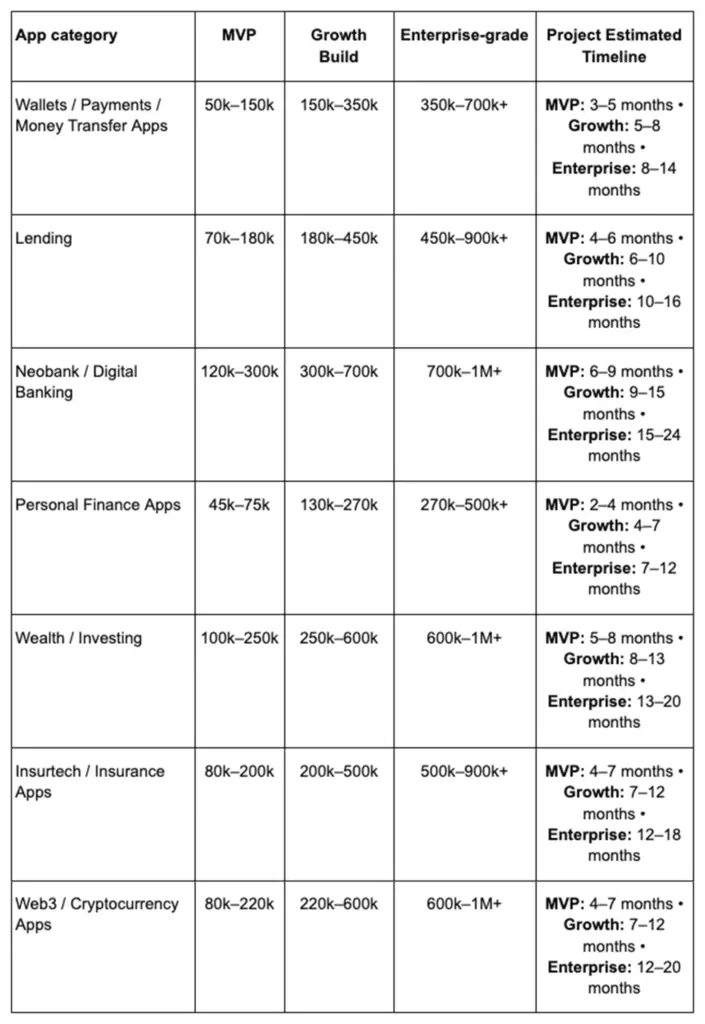

Wallets and Payment apps: $50K–$150K

Lending apps: $70K–$180K

Wealth / Investing apps: $100K–$250K

Neobank / Banking apps: $120K–$300K - A realistic budget is not just build cost. Engineering can take 40–60% of spend, QA and hardening 15–30%, security 5–20%, and year-one maintenance often adds 15–25% annually.

- KYC, money movement, audit trails, and admin tooling usually push budgets up fastest because they add edge cases, operational workflows, and audit-ready requirements.

- If a quote falls far below the planning ranges, it often means critical work like security testing, QA hardening, ops tooling, or partner readiness has been left out.

Estimating fintech app development cost is not just about choosing a number from a pricing range. It is about budgeting for product scope, compliance exposure, third-party integrations, and the long-term operating reality after launch.

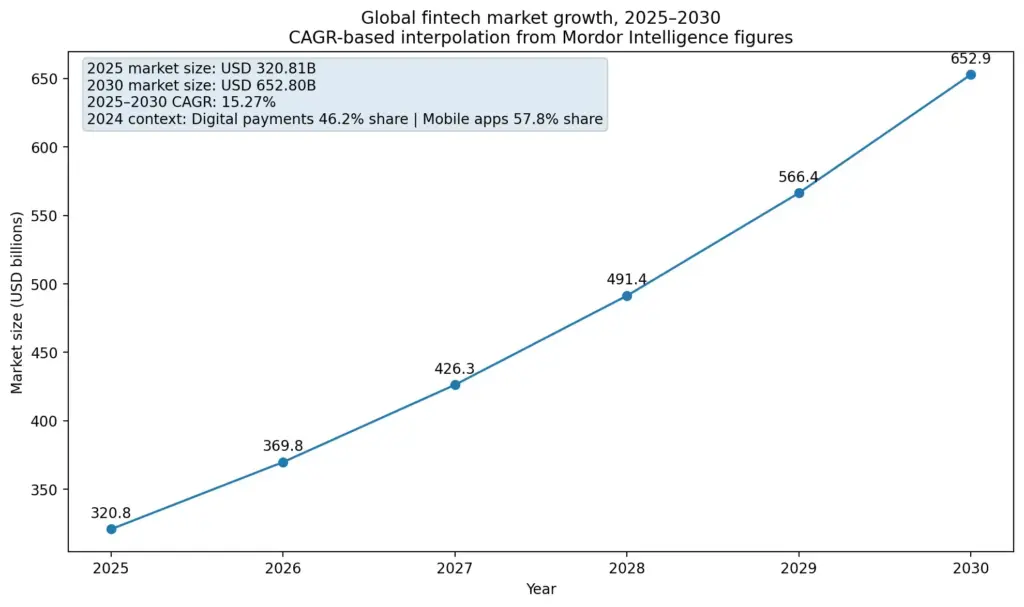

It matters even more in a market Mordor Intelligence values at USD 320.81 billion in 2025 and expects to reach USD 652.80 billion by 2030, with digital payments and mobile applications leading a large share of fintech activity.

In other words, cost planning now sits inside a fast-scaling, mobile-first, integration-heavy environment.

This guide explains where budgets typically go, how costs shift across fintech categories, and which modules tend to push spend up fastest, from KYC onboarding to money movement, audit trails, and risk controls.

Fintech App Development Cost: What You’re Actually Paying For

Budgeting gets easier when you separate what you build, what you must prove, and what you must run.

The Three Layers Of Fintech Cost

- Build effort – The visible work: mobile apps, backend services, admin tooling, and QA cycles. This is core feature development (logic, UI, databases, APIs, integrations). For example, Andersen finds core dev often takes ~45–55% of the budget. Underestimating it leads to scope creep; clarifying platforms (iOS vs Android vs web) and integration count is key.

- Compliance/Security effort – The “must-have” layer that protects financial data and satisfies regulators or partners. This includes requirements like encryption, KYC/AML flows, audit logs, and penetration testing. These tasks aren’t optional extras – they’re integral. For instance, many teams reference OWASP’s MASVS as a baseline for mobile fintech security. Ignoring these adds “future rework tax.” Modern Treasury warns that “audit trails take engineering cycles that could go toward features”, so it pays to build security within now (e.g. threat modeling, penetration tests, and remediations upfront). This layer can easily add 20–30% extra to the baseline budget.

- Operational run rate – Post-launch costs like hosting, monitoring, on-call support, and recurring vendor fees. These scale with usage. For example, identity checks or payment transaction fees are typically per-use. If Stripe Radar fraud screening costs ~$0.05–$0.10 per transaction, a higher transaction volume directly increases your monthly bills. Set aside a budget for cloud infrastructure (auto-scaling, logging), ongoing regulatory reports, and vendor subscriptions. Andersen notes maintenance often ends up ~15–25% of the initial build cost annually. Vendor fees (per-check or per-user) will also rise as customers grow.

For context, vendor hourly rates vary widely by region (e.g. roughly $20–$50/hr in India/Eastern Europe vs. $100–$200/hr in North America). This is why specifying scope and deliverables matters more than quoting any “average rate.” If a fintech quote looks unusually low, ensure it hasn’t excluded essential work (like security testing or administrative tooling).

Why Fintech Estimates Vary More Than “Regular Apps”

Fintech products have a larger risk surface: identity, fraud, and money movement add edge cases (fails, retries, disputes, reversals) plus back-office ops.

Regulatory expectations around AML/CFT are influenced by global standards such as the FATF Recommendations (updated in October 2025).

Identity is also deeper than “email + password.” NIST’s digital identity guidelines (SP 800-63-4) describe technical requirements for identity proofing and authentication assurance, which shapes how strict onboarding and login flows must be.

What To Collect Before Estimating

Before asking vendors for a number, gather a clear scope brief. A practical rule: if a quote seems “too good,” check what’s excluded. Prepare a one-page project brief including:

- Primary user journeys & edge cases – List core flows and failure states (e.g. login, transfer, payout, and what happens on error).

- Launch regions & regulations – Target countries and data residency rules (this determines KYC rules, currency support, etc.).

- Money movement scope – Will you transfer funds, issue cards, or just display account data? The more movement and PCI scope (card payments) you include, the higher the cost.

- Integration list – Enumerate needed third parties (payment processors, banking APIs, KYC/AML providers, fraud engines, messaging/analytics tools). Each integration adds effort and testing.

- Non-negotiables – Any fixed requirements, e.g. compliance baseline (PCI, SOC 2), uptime targets, or a strict launch timeline.

How Much Does It Cost to Build a FinTech App?

Before diving into the details, let’s start with a general cost overview for building a FinTech app. These estimates are based on previous project experience and calculated using an average hourly rate of $50, which is common in Central and Northern Europe. They represent rough MVP budget ranges for some of the most common FinTech app categories, including banking, lending, investment, insurance, and personal finance.

The table below provides approximate time and cost ranges for different types of FinTech apps, giving you a practical baseline before moving into the detailed breakdowns.

Also Read: How Much Does AI App Development Cost?

Types of Fintech Applications and Their Cost Estimates

Category benchmarks help you sanity-check quotes—then ask why your scope is above or below the baseline.

Several 2026-focused fintech guides describe MVPs starting in the tens of thousands of dollars and scaling into the hundreds of thousands (or more) as you add regulated onboarding, money movement, and heavier controls.

Fintech App Development Costs by Solution Type And Complexity Tier

Note: Use the table as an early-screen tool—not a quote. If a fintech app development cost quote is far below these ranges, it often means key work is excluded (security testing, QA hardening, ops tooling, or partner readiness).

Wallets, Payments and Money Transfer Apps (Money Movement + Fraud Controls)

Money movement and fraud controls are key here. Expect an MVP wallet app in the $50K–$150K range, growing to $150K–$350K+ as you add multiple currencies, higher volume, or PCI-level card flows. For example, Andersen notes simple payment apps often start ~$40–90K MVP, before scaling.

If a quote is far below these ranges, it usually means critical work (like fraud handling or compliance) was omitted.

Lending (Underwriting Workflows + Data Providers)

Loans and credit apps need underwriting workflows and many data providers. A basic lending app (e.g. simple loan offers) might be $70K–$180K for MVP. Full-featured lending (with credit scoring algorithms, bank API checks, extensive KYC/AML) often runs $180K–$450K or more.

Our sources show average lending apps from ~$40K up to $400K+ depending on complexity. Key cost drivers are credit bureau integrations and regulatory/legal review.

Neobank/Digital Banking (Core Banking Dependencies + Higher Integration Load)

Such digital-only banks connect to core banking systems and have many integrations. Even an MVP neobank app can be $80K–$150K, with a production-grade solution easily exceeding $200K–$300K.

The main costs: core banking integration, compliance (KYC, reporting), multi-account logic, and often multiple platform support.

Personal Finance Apps

Personal finance apps usually sit at the lower end of the fintech range. A basic budgeting or expense-tracking MVP can fall around $45K–$75K, while more advanced personal finance products often move into the $130K–$270K range.

Costs rise when you add bank account aggregation, recurring sync, bill reminders, AI-driven spending insights, shared planning features, or investment tracking. Since these apps usually focus more on visibility and planning than regulated money movement, they often carry less compliance weight than payments, lending, or neobank products.

Wealth / Investing Apps (Real-Time Data + Suitability/Audit Trails)

Real-time data feeds and suitability/audit features dominate. Expect $100K–$250K for a secure trading or robo-advisor MVP, scaling to $250K–$600K+ for a polished brokerage-grade platform.

High-frequency updates and regulatory filings (like automated audit logs for trades) add complexity.

Insurtech / Insurance Apps (Claims/Document Workflows + Partner Systems)

Claim/document workflows and back-end partner integrations drive costs. A simple insurance quote-and-claim MVP might be $80K–$200K, but a full insurance management system can go $200K–$500K+.

Handling all claim edge cases and legacy policy systems typically pushes insurance apps toward the higher end.

Web3 / Cryptocurrency Apps (Custody Model + Key Management Implications)

Wallet custody and key management are costly. Crypto/Web3 MVPs often start around $80K–$220K, rising to $220K–$600K+ for exchange/custody features.

The security model (custodial vs non-custodial) and blockchain integrations determine much of the cost. For example, hardware-level encryption and multi-sig wallets can significantly raise development effort.

Factors That Influence Fintech App Development Cost

No single variable decides fintech app budgets. Cost usually shifts based on scope, platform decisions, compliance exposure, delivery model, and the long-term support the product will require after launch.

Product Requirements And App Complexity

Scope is still the biggest cost driver. A fintech app with one core journey and a limited integration set will cost far less than a product with multiple user roles, money movement, auditability, and exception-heavy workflows.

Platform Choice And UI/UX Scope

Platform decisions change both build effort and QA scope. A single-platform MVP is easier to fund than launching on iOS, Android, and web together, especially when biometrics, secure storage, and recovery flows are involved.

Compliance, Regulations, And Security Level

The more regulatory exposure a product carries, the more it costs to build and validate. KYC, AML, PCI scope, audit trails, and security testing all increase effort, but leaving them vague usually creates more expensive rework later.

Development Partner Location And Team Model

Rates vary by region, but the cheapest team does not always produce the lowest total cost. Delivery experience, planning quality, and ownership model often matter more than hourly price alone.

Tech Stack And Advanced Technologies Used

The stack affects both delivery speed and long-term maintainability. AI features, blockchain integrations, real-time analytics, and advanced fraud tooling can improve capability, but they also raise implementation and testing effort.

Top Technologies in Fintech Application Development

Common technologies in fintech app development include:

- AI and machine learning for fraud detection, risk scoring, and personalized financial insights

- Blockchain for custody models, transaction verification, and crypto-focused product flows

- Biometric authentication for stronger login security and identity verification

- Real-time analytics for dashboards, reporting, and operational visibility

- Cloud-native infrastructure for scalability, availability, and long-term operational control

These technologies can strengthen product capability and user trust, but they also tend to increase implementation effort, testing scope, and long-term maintenance requirements.

Also Read: Flutter vs Native App Development: Choosing The Right Technology

Post-Launch Support And Maintenance

The budget does not stop at launch. Monitoring, infrastructure, vendor changes, security patches, and ongoing support all add recurring cost, which is why maintenance should be planned as part of the original budget.

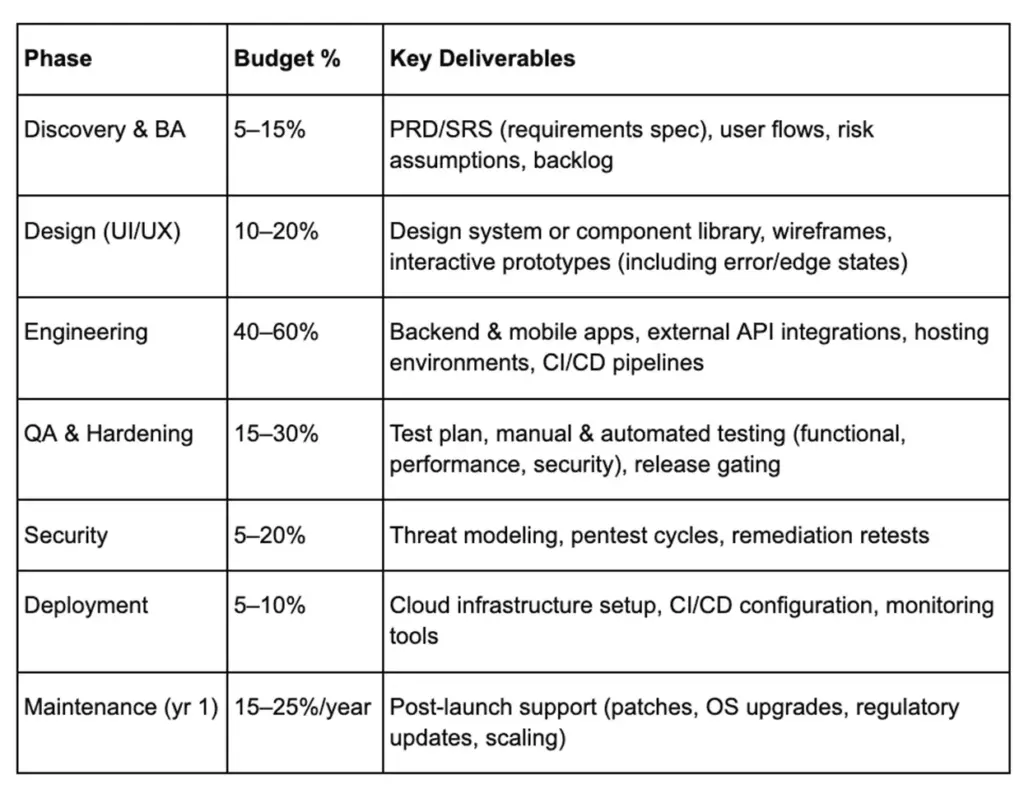

Fintech App Development Cost Breakdown By Phase And Deliverables

A clear phase-based breakdown ties budget to real deliverables (not just hours). Rough percentage ranges (subject to project specifics):

- In Discovery, the goal is clarity. Deliverables should include a complete requirements spec (PRD/SRS) and user flows with failure states, as well as a backlog of features/tasks. This “DNA” of the project greatly reduces rework.

- In Design, outputs that cut build time are a living design system, full-fidelity prototypes (for core and error flows), and detailed states (e.g. confirmations, error messages). These ensure developers don’t waste time on UI guesswork.

- In Engineering, clarify scope early (how many platforms, how many dev/test environments, how automated your pipeline is). More backend complexity (multiple services, high volumes) increases cost. Setting up CI/CD and staging environments here saves headaches later.

- In QA, deliverables include a formal test plan, coverage matrix (OS/devices), and automation scripts for regression. Don’t skimp on security testing. Use OWASP MASVS/MASTG to define mobile security test cases. Early automation of critical flows (in CI) cuts long-term maintenance costs.

- Finally, include a handover package: technical documentation, API docs, deployment/runbook, and training for operational teams.

Vendor Quote Checklist: When comparing quotes, ensure each lists the above deliverables, plus assumptions/exclusions (platforms, environments, deliverable definitions).

How Much Do Fintech Software Development Key Features Cost?

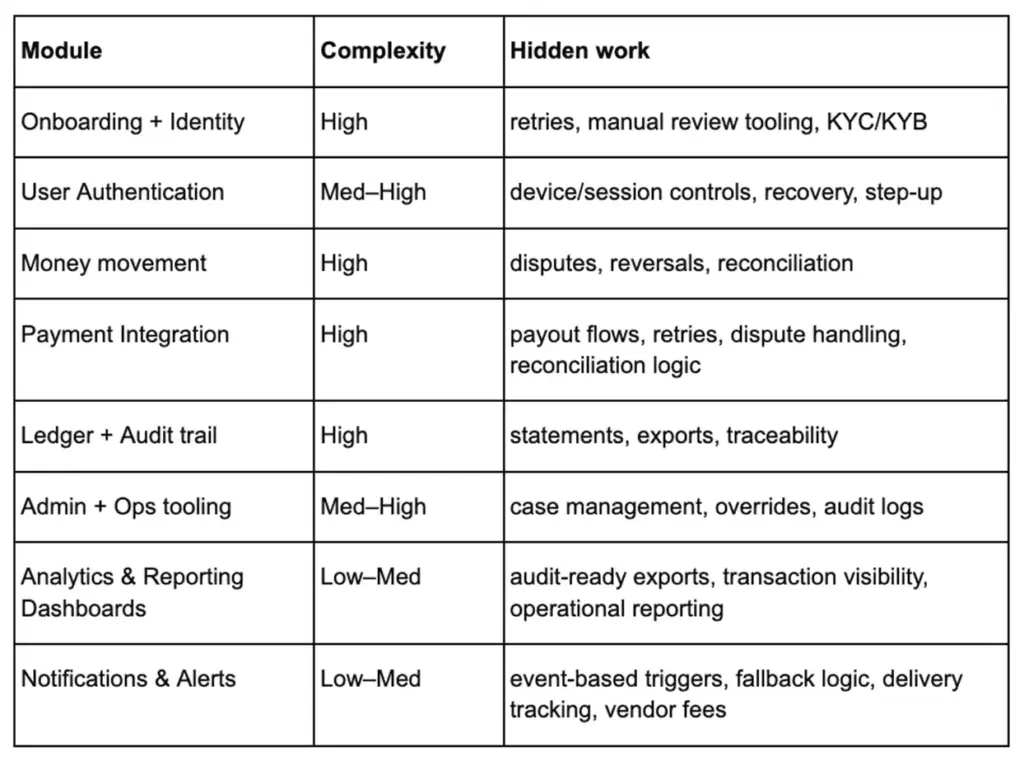

For fintech budgeting, modules that touch identity, money movement, and auditability tend to inflate budgets because they create edge cases and operational workflows. In practice, fintech app development cost increases fastest when these modules require manual review tooling and audit-ready records.

Quick Cost Heatmap

Each of the above modules should prompt a cost discussion. For instance, integrating a KYC provider not only costs in initial dev, but also requires building UI for exceptions (failed matches) and infrastructure for identity data. Likewise, “money movement” might seem simple, but dispute and chargeback handling can double the work. Always evaluate these modules as multi-step features, not just “one-off” forms. Let’s discuss them a little further.

Onboarding + Identity

NIST’s digital identity guidelines describe identity proofing and authentication requirements; in product terms, that becomes doc capture quality checks, selfie/liveness steps, retries, and fallbacks.

Many providers price per completed verification; Stripe Identity publishes pay-as-you-go per-verification pricing.

User Authentication

Authentication cost is mostly recovery + session security. OWASP MASVS is often used as a baseline to turn those needs into verifiable mobile controls.

Money Movement

Money movement needs safe retries, clear transaction states, reversals, and dispute workflows. Platform models can add ongoing fees (per active user / per payout), affecting unit economics.

Payment Integration

Payment integration is rarely just one API connection. Costs usually grow with payout flows, retries, dispute handling, reconciliation logic, and support for multiple rails or processors, which is why this module often becomes one of the heavier build areas in a fintech product.

Ledgering + Audit trail

Ledger costs rise when you need statements, exports, reconciliation, and immutable “who changed what” history for investigations. This module alone can shift budget forecasts because reporting requirements are rarely “one and done.”

Admin Console & Ops tooling

Admin tooling is the bridge between “edge cases” and reliable operations. SOC 2 is commonly used to communicate internal control assurance, which makes permissions and audit logs core scope.

Analytics & Reporting Dashboards

Analytics and reporting dashboards cost more when the product needs audit-ready exports, transaction visibility, operational reporting, and admin-side decision support instead of basic charts. A light dashboard may stay manageable, but deeper financial reporting usually increases backend logic, data modeling, and QA scope.

Notifications & Alerts

Notifications look simple, but they add cost once the product needs event-based triggers, delivery tracking, fallback logic, and compliance-aware messaging. They also create recurring run-rate impact, since tools like SMS and email providers typically charge by usage, and those “small fees” scale with customer activity over time.

Compliance & Security Workstreams That Must Be Budgeted Explicitly

If your estimate doesn’t separately budget compliance and security, it’s probably incomplete. Key items to account for:

- When PCI DSS applies – Any cardholder data (even tokenized) triggers PCI scope. PCI DSS brings technical requirements (data encryption, strict access controls, network segmentation) and audit obligations. For a fintech MVP that touches cards, plan for building all PCI controls and paying for an assessor. Industry sources note annual PCI compliance can run tens of thousands per year (e.g. ~$15K–$50K). Even using third-party payment processors, you’ll likely need a QSA review at some threshold. Importantly, tokenization or vaulting must be done correctly to shrink scope, otherwise you still pay.

- OWASP MASVS as a baseline – For mobile fintech apps, many teams treat OWASP MASVS as a de facto checklist. MASVS covers secure storage, strong crypto, reverse engineering resistance, and more. Planning to meet MASVS (and its companion MASVS Testing Guide) from day one helps avoid costly late fixes. For instance, embedding SSL pinning and hardware-backed key storage will add initial cost but save expensive refactoring.

- Security testing line items – Explicitly include threat modeling and penetration testing in your quote. Threat modeling (often a workshop or review) can catch architectural flaws early at low cost. At minimum, budget one formal pentest cycle (coding fix + retest). For fintech, two pentests (pre-launch and post-launch) are common, plus vulnerability scanning. Each cycle (with a reputable firm) can cost several thousand dollars, plus your dev hours to fix issues. Andersen’s analysis shows that QA/security can take ~20% of a project’s effort.

- Compliance as a timeline risk – Regulatory approvals and audits can delay a project independently of coding. Collecting compliance evidence (e.g. audit logs, traceability matrices) takes time. For example, Deloitte notes that fintech companies now face intensive operational audits and must build formal risk programs. Factor these into your schedule: e.g. obtaining certification (PCI/SOC2) may require working through an external checklist.

Compliance Scope Checklist

As a practical aid, clarify upfront:

- Payments scope (PCI) – Will your app store/transmit card data? If yes, what PCI level certification is needed?

- Identity depth (KYC/KYB + AML) – What ID verification level is required for your user base? How many screening checks per user?

- Audit requirements – Do regulators or partners demand detailed logs and retention? (e.g. 5+ years of transaction history.)

- Security baseline – Are there known controls or standards (MASVS, OWASP Top10, privacy laws) you must implement and prove?

Integrations And Vendor Stack Costs

Integrations often determine final cost because they add both development effort and recurring expenses. Key areas are as follows:

- Banking/Payment Rails & Aggregators – Each bank API or payments platform (ACH, SWIFT, card issuer) requires separate integration, testing, and monitoring. Andersen highlights that “integration count multiplies QA and maintenance” (each service’s updates and quirks cost in the long run). Also consider usage pricing: many partners charge monthly or per-transaction. For instance, some embedded accounts platforms may charge per active user or per payout. These fees directly add to your run-rate. Planning tip: start with essential rails and design your code so you can add more integrations later without rewriting core logic.

- Identity/KYC Vendors & AML Screening – Implementation vs per-check fees. Account for both: it might cost ~$15K–$30K to integrate a KYC SDK, plus ~$1–$2 per identity verification. Similarly, AML screening services charge per check (often a few cents each). Don’t forget monthly minimums or verification timeouts. Over time, high-volume clients can spend heavily on identity checks, so treat this as an ongoing cost.

- Fraud & Risk Tooling – Tools like Sift, ThreatMetrix, or device intelligence APIs usually price per transaction or as a subscription. Integrating a fraud rules engine also involves dev work (setting rules, training the model). For example, Stripe’s Radar is ~$0.05–$0.10 per transaction screened, plus ~$25 per dispute handled. Factor these into your per-transaction cost model. Remember that tuning fraud systems (minimizing false positives) can be an iterative cost after launch.

- Messaging, Analytics, and Support Tools – These are the “small fees” that compound. Twilio/SMS, SendGrid/email, analytics platforms (Mixpanel), and customer support tools all typically charge by usage. For example, Twilio may charge ~$0.01–$0.05 per SMS. While trivial initially, these costs scale linearly with users. Budget them as a percentage of server/cloud spend, and plan to review actual usage after launch.

Vendor Strategy Tip: Start with the minimum viable stack. Abstract vendor-specific code behind interfaces (so you can switch providers if terms change). Ensure each integration has a clear owner and a rollback/alternate plan.

Team Model, Platform Choices & Delivery Approach

Team model drives fintech app development cost variance because it changes speed, quality, and predictability. The same scope can cost very different amounts depending on in-house vs agency vs hybrid delivery.

Typical Team Roles By Stage

Lean fintech builds still need product, design, mobile, backend, QA, DevOps, and security. Rate benchmarks vary, but Clutch’s 2026 guide reports many app development companies in a $25–$49/hour band and emphasizes scope as the main driver.

Platform Strategy Tradeoffs (iOS/Android/Native Vs Cross-Platform)

Native can reduce platform risk for performance/security-critical features but costs more if you build iOS and Android separately. Cross-platform can reduce duplicated UI work, yet you still need platform-specific QA and secure storage integrations.

Agile Vs Fixed-Scope For Fintech

Fixed-scope estimates can break when partner onboarding or compliance requirements surface late. Agile delivery improves reliability when milestones are defined as testable deliverables. DevOps guidance around deployment frequency often highlights that smaller, more frequent releases reduce risk per change and speed feedback loops.

This is why teams often treat fintech app development cost as a sequence of milestones, not a single quote.

How To Read A Proposal And What “Maintenance” Really Includes

Watch for hidden exclusions (security testing, app store release overhead, SLAs) and vague “maintenance” definitions. If “AI acceleration” is promised, treat it as tooling—not a replacement for governance. GitHub’s Copilot research highlights productivity benefits, while NIST provides an AI Risk Management Framework for thinking about AI-related risks in development workflows.

Practical tip: Ask for a written assumptions list (what’s included vs excluded), a test strategy summary, and a handover plan. The said three artifacts prevent “quote drift” when requirements evolve. Also confirm who owns store submissions, security retesting, and on-call coverage—these items often slip between “build” and “run” responsibilities upfront and in writing.

Post-Launch Costs, Publishing Requirements, And Maintenance Planning

The initial build is only part of the fintech app development cost picture. You also need a budget for publishing, operations, and ongoing maintenance.

App Publishing Prerequisites As Checklist Items (Apple Developer Program, Google Play Console)

Publishing fees are small but predictable:

- Apple Developer Program: 99 USD per membership year.

- Google Play Console: US$25 one-time registration fee.

Beyond fees, you must budget developer time for store compliance i.e. preparing privacy disclosures, security statements, and responding to review feedback, etc.

While release overhead (store policies, privacy disclosures, QA cycles) is usually the larger cost.

Monitoring And Incident Response

Fintech apps typically promise high availability (finance users expect instant responses). Plan for continuous monitoring (logs, alerts) and an incident response framework.

Google’s SRE practices are a good model: define error budgets, set up on-call rotations, and practice postmortems.

Having basic SLAs and real-time alerts (for failed transactions or downtime) should be in your plan. While initially “only” a few percentage points of effort, this can save huge costs from undetected issues later.

Maintenance Categories

Post-launch, the budget falls into categories: OS and dependency updates (new iOS/Android versions), security patching, regulatory changes (e.g. new AML rules), performance tuning, and minor enhancements.

Standards like ISO/IEC 14764 (Software Maintenance) even outline that maintenance should be planned as part of the project lifecycle.

Andersen data confirms that annual maintenance is often ~15–25% of the original build cost. So if your project was $100K, expect $15K–$25K/year in upkeep under normal growth.

Recap of Hidden Fintech App Development Costs To Watch For

Don’t forget periodic audits (PCI DSS, SOC 2, GDPR reports). Infrastructure scaling: e.g. AWS/Azure costs can grow non-linearly with a user base. Vendor fees: every identity check, SMS message, and analytics event is paid per use. And support tools (like CRM seats, Sentry/Datadog plans) rise with team and usage. These often hide in “Opex” but should be planned.

How to Build a Fintech Application? A Practical Step-by-Step Process for Building a Fintech App

A fintech app build usually moves faster and more cleanly when the team treats it as a sequence of milestones instead of one large delivery block. The goal is to define risk early, keep the first release narrow, and avoid expensive rework once integrations, compliance, and launch requirements start expanding.

Discovery & Research (3–5 days)

This stage is about getting the brief right before development starts. The team defines the core user journey, maps edge cases, confirms launch regions, lists integrations, and identifies the compliance and security assumptions that will shape the rest of the build.

UI/UX Design (10–15 days)

Once the scope is clear, the next step is to design the core flows and the states around them. In fintech, that usually means not just primary screens, but also retries, failures, approvals, locked states, and recovery journeys that reduce confusion later in development and QA.

MVP Development (30–50 days)

This is where the first working version takes shape. The team builds the core product flow, connects the required integrations, sets up environments, and focuses on the features that prove the main use case without expanding into unnecessary modules too early.

Testing & Quality Assurance (5–10 days)

QA should validate more than basic functionality. For a fintech MVP, testing should cover critical flows, integration behavior, edge cases, security-sensitive scenarios, and release readiness so the product does not reach launch with unstable logic or avoidable compliance gaps.

Launch & Support (ongoing)

Launch is the start of the operating phase, not the end of the project. Once the product is live, the focus shifts to monitoring, incident response, fixes, dependency updates, vendor changes, and small improvements that keep the app stable as usage and operational demands grow.

Challenges in Fintech App Development Process

Fintech products are harder to build than standard apps because the challenge is not just shipping features. Teams also have to manage compliance exposure, integration risk, security expectations, and the operational demands that come after launch.

Regulatory Complexity And Changing Requirements

Regulatory scope can change the build more than teams expect. A product may begin with a narrow feature set, then expand once KYC depth, auditability, data handling, or regional compliance requirements become clearer.

That usually affects both timeline and cost. What looked like a simple product flow can quickly turn into a regulated workflow with more validation, documentation, and review points.

Third-Party Dependency And Integration Risk

Many fintech apps depend on payment processors, banking APIs, KYC vendors, fraud tools, and messaging platforms. Each dependency adds implementation work, but it also adds failure states, monitoring needs, and long-term maintenance.

This creates delivery risk as well. A strong internal build can still get delayed if a vendor changes requirements, has unstable documentation, or needs more testing than expected.

Security, Fraud, And Trust Expectations

Fintech users expect the product to feel secure from the first interaction. That means teams have to think beyond login screens and cover encryption, session controls, fraud signals, permissions, and audit-ready access patterns.

The challenge is that security work often cuts across the whole product. It is not one feature to “add later,” which is why weak early planning usually becomes expensive rework.

Testing Edge Cases In Money Movement Workflows

Money movement creates more exceptions than most app teams expect. Retries, failed states, reversals, disputes, duplicate actions, and delayed confirmations all need to be handled clearly across both product logic and user experience.

That makes QA harder too. Teams are not just testing happy paths. They are testing what happens when real financial actions fail, repeat, or arrive out of sequence.

Balancing Speed To Launch With Compliance Readiness

Most teams want to move fast, especially at MVP stage. The challenge is deciding how lean the first release can be without creating a product that has to be reworked once security, compliance, or partner expectations catch up.

The best fintech builds usually do not start with the biggest scope. They start with a narrower flow that still preserves a compliant path forward.

Scaling Operations After Release

Launch does not remove complexity. It shifts it into operations, where uptime, support, monitoring, vendor coordination, and incident response start affecting the real cost and reliability of the product.

As usage grows, small operational gaps become bigger problems. That is why fintech teams need to plan for scale, not just in infrastructure, but also in workflows, ownership, and support readiness.

Tips and Tricks to Reduce the Fintech App Development Cost

Reducing fintech app development cost is not about cutting critical work. It is about making better decisions early, keeping the first release focused, and avoiding choices that create rework once compliance, integrations, and scale become more demanding.

Prioritize App Features

Not every feature belongs in the first release. The smartest way to control budget is to identify the features that directly support the core user journey and delay lower-impact modules until the product proves traction.

This matters even more in fintech, where each extra feature can add testing effort, operational workflows, and compliance implications. A smaller but better-scoped feature set usually leads to a more stable and cost-efficient launch.

Focus on MVP Development

A narrow MVP is one of the most reliable ways to reduce cost without weakening the product. It helps teams validate the core use case first instead of funding a broader roadmap before the market has confirmed what users actually need.

The key is to keep the MVP lean without breaking the future path. If the first version still respects security, compliance, and integration realities, it is far easier to expand later without paying a rebuild cost.

Choose the Framework Wisely

Framework and platform choices affect both build speed and long-term maintenance. In some cases, cross-platform development can reduce duplicated UI work and shorten early delivery, while in other cases native development is the safer choice for performance, device-level security, or platform-specific features.

The cost-saving decision is not always the cheapest stack on paper. It is the one that supports your product goals without creating unnecessary complexity or future migration pressure.

Strategic Team Collaboration

Budget efficiency improves when the right people are involved at the right stage. Clear coordination across product, design, engineering, QA, DevOps, and security reduces misalignment and helps teams catch scope or delivery issues before they turn into expensive delays.

This is especially important in fintech, where a missed dependency or vague requirement can affect more than one workstream at once. Better collaboration usually means fewer handoff gaps, cleaner execution, and more predictable delivery.

Adopt Agile Development Process

Agile delivery helps control cost by breaking the build into smaller milestones instead of treating the project as one fixed block. That gives teams more room to validate assumptions early, adjust priorities, and catch complexity before it spreads across the whole roadmap.

For fintech products, that flexibility is valuable because requirements often shift once integrations, partner reviews, or compliance details become clearer. Smaller releases and milestone-based planning usually make costs easier to manage than rigid scope assumptions.

Conclusion

Fintech app development cost is not a fixed number. It is the result of scope, integrations, compliance exposure, security requirements, and ongoing operational run rate.

The more clearly you define those variables early, the easier it becomes to compare vendor quotes, defend budget decisions, and avoid hidden costs later.

Instead of chasing the cheapest estimate, focus on deliverables, risk coverage, and long-term maintainability.

A well-scoped roadmap, the right vendor stack, and early investment in security usually lead to a more predictable and sustainable fintech build.

How can BrainX Help in Fintech Application Development?

Fintech projects get expensive when scope, compliance, and vendor decisions stay vague for too long. Our leading fintech app development service company helps teams turn those variables into a clearer delivery plan through structured discovery, secure architecture thinking, and realistic milestone planning. The goal is not just to estimate faster but to reduce hidden costs, avoid rework, and move toward launch with better budget control.

Ready to build the next breakthrough in Fintech

Connect with our experts today to explore more!

FAQs For Fintech Budgeting And Estimates

What’s the minimum budget for a fintech MVP?

The minimum budget for a fintech MVP depends on how narrow the first release is. A lower-cost MVP usually assumes one core user journey, limited integrations, a smaller launch region, and only the compliance controls needed for that product scope. As soon as you add KYC, money movement, fraud checks, or deeper admin tooling, the budget increases.

What is fintech app development cost per month?

Fintech app development cost per month depends on the stage of the product. During development, monthly costs usually include design, engineering, QA, DevOps, security work, cloud infrastructure, and vendor tools. After launch, monthly spend typically shifts toward maintenance, monitoring, support, usage-based vendor fees, and ongoing product updates.

How long does it take to build a fintech app?

The timeline depends on scope, integrations, compliance requirements, and testing depth. A lean MVP can move faster, but production-ready fintech products usually take longer because partner onboarding, security reviews, and release preparation often add more time than teams expect.

Does publishing a fintech app add extra cost?

Yes, but the account fees are usually the smallest part of the expense. The larger cost usually comes from release preparation, store compliance, privacy disclosures, QA cycles, and the developer time needed to handle submission requirements and review feedback.

What does annual fintech app maintenance usually include?

Annual maintenance usually covers OS updates, dependency upgrades, security patches, infrastructure updates, vendor API changes, monitoring, bug fixes, and smaller product improvements. It should also include the time and budget needed to keep the product stable as compliance, platform rules, and user expectations evolve.