Claims leaders do not need another vague promise that AI will transform insurance. They need a credible path to lower operating expenses, reduce leakage, shorten cycle times, and improve customer outcomes without creating governance problems or disrupting core systems. That is why intelligent automation in insurance has become a priority in 2026.

Insurers face rising repair costs, claims inflation, fraud, catastrophe exposure, and growing expectations for digital service. Yet many carriers remain caught between successful experiments and enterprise-wide adoption.

The savings potential is real, but no single percentage applies to every carrier or workflow. Results depend on the line of business, process maturity, data quality, integration complexity, and the share of claims that can safely move through touchless or touch-light handling.

McKinsey’s Claims 2030 analysis cites lower claims-processing costs and reduced adjustment expenses as key benefits of AI-enabled claims management. Capgemini’s World Property and Casualty Insurance Report 2026 cautions that 40% of P&C leaders say AI meets expectations, yet 42% have not measured AI outcomes, and many report only marginal gains.

The insurers seeing the strongest results treat automation as a claims operating model upgrade, not simply a technology rollout.

Key Takeaways

- Savings come from connected levers: Fewer manual touchpoints, shorter cycle times, lower leakage, more precise fraud detection, and reduced escalation costs.

- Intelligent automation goes beyond RPA: The stack includes workflow orchestration, intelligent document processing, machine learning, computer vision, LLMs, integrations, and human-review controls.

- The best starting points are narrow and measurable: FNOL intake, low-complexity triage, document extraction, fraud scoring, and proactive customer communication.

- Governance must be built into the workflow: Confidence thresholds, audit trails, source-linked outputs, human approvals, and continuous monitoring are essential.

- Finance-grade measurement starts before deployment: Baseline cycle time, touchless rate, reopen rate, leakage, contact volume, and SIU referral precision.

- Build versus buy requires a hybrid approach: Buy proven commodity capabilities, but customize policy-aware decisioning, orchestration, integrations, and governance.

What “Intelligent Automation” Means in Insurance Claims (Beyond RPA)

RPA still plays a useful role in insurance, but it is no longer sufficient for the most expensive claims activities. Claims work involves unstructured documents, incomplete narratives, images, policy interpretation, fraud signals, customer communication, and judgment calls that must remain defensible.

Modern intelligent automation insurance programs combine workflow, rules, data, AI services, and human controls. Instead of assigning every claim to an adjuster by default, insurers create a triage layer that evaluates complexity, severity, confidence, and risk before deciding how the claim should proceed.

The result is not automation for its own sake. It is a more controlled operating model in which routine work moves quickly and human expertise is reserved for claims where it can materially improve the outcome.

Intelligent Automation Insurance (Definition, Scope, and What It Replaces)

Intelligent automation in insurance refers to combining workflow orchestration, APIs, RPA, intelligent document processing, machine learning, LLMs, and computer vision to complete claims activities with measurable controls.

It extends traditional automation in two important ways. First, it can interpret unstructured information such as emails, PDFs, images, notes, invoices, and call transcripts. Second, it can support routing and decision-making based on confidence, severity, policy rules, and risk signals.

Its scope can cover the entire claims lifecycle:

- Front office: FNOL capture, identity verification, coverage checks, initial triage, and reserve recommendations

- Middle office: Document ingestion, billing review support, subrogation signals, vendor coordination, and investigation

- Back office: Payments, recoveries, compliance documentation, reporting, and audit support

In practice, it replaces swivel-chair work such as copying information between systems, manually sorting attachments, eliminating duplicate notices, looking up policy details, and preparing routine claim summaries.

What it does not replace is the adjuster. AI supports interpretation, prioritization, and routing, while policy logic, workflow rules, and human approvals enforce the final controls.

What’s Driving Adoption Now: Cost Pressure, Customer Expectations, and Data Readiness

The commercial pressure is straightforward. Claims organizations are absorbing higher repair costs, inflation, supply-chain disruption, catastrophe exposure, and more complex losses. Operational inefficiency can no longer be offset through pricing alone.

Customer expectations are also changing. Policyholders increasingly compare their claims experience with real-time e-commerce tracking and digital banking. When information is unclear, customers call more often, satisfaction declines, and a manageable claim can become a complaint or retention problem.

Capgemini’s 2026 P&C report shows how wide the execution gap remains. Many insurers report only marginal gains, 42% have not measured AI outcomes, and most initiatives remain at the proof-of-concept stage. The same research found that 72% of AI spending goes to technology and only 28% to change management.

The third driver is data readiness. Claims teams can now combine structured policy records with telemetry, photos, video, invoices, correspondence, connected-device signals, and historical outcomes. Insurers can also use mature OCR, document extraction, vision, and language capabilities without training every component from scratch.

Together, these pressures have made intelligent automation insurance a practical operating priority rather than a long-term experiment.

Where Claims Cost Reduction Really Comes From

Stop treating “AI savings” as one cost bucket. The business case becomes clearer when the claims P&L is broken into the areas automation can actually change.

A useful business case separates claims costs into four categories:

- Operating expense: Adjuster time, call handling, document review, administrative work, and vendor coordination

- Leakage: Overpayments, missed policy conditions, inconsistent reserves, weak recoveries, and processing errors

- Fraud waste: Claims or claim elements that should have been investigated, reduced, or declined

- Escalation cost: Complaints, litigation, supplements, reopenings, and long-tail handling overhead

McKinsey’s Claims 2030 analysis points to lower claims-processing costs and reduced adjustment expenses as important benefits of AI-enabled claims operations. The same analysis emphasizes that value comes from combining digital tools, automation, analytics, and human expertise rather than relying on one model or isolated workflow.

The savings potential is real, but no single percentage applies to every carrier or workflow. The strongest results come from combining lower handling expense, fewer manual touches, reduced leakage, better fraud prioritization, and fewer avoidable escalations. Each insurer should establish its own target through baseline measurement and a controlled pilot.

Claims Operating Cost Model: Cycle Time, Touchpoints, Leakage, and Severity

A useful cost model starts with five operational variables:

- Cycle time: Time from FNOL to settlement, including waiting time between activities

- Touches per claim: Human actions required to move the file forward

- Leakage rate: Avoidable overpayment and missed recovery opportunities

- Severity drivers: Supplements, delayed mitigation, poor estimates, and vendor rework

- Reopen rate: A measure of closure quality and claim completeness

Cycle time compounds. A slow claim generates more customer contacts, more administrative work, longer reserve periods, and a greater risk of disputes.

Touchpoints create similar problems. Every handoff is another opportunity for delay, error, and lost context. Removing two unnecessary handoffs often produces more value than making one existing handoff slightly faster.

Leakage and severity require different controls. Automation can validate policy limits, identify duplicate payments, surface missed recoveries, detect unusual billing, and flag inconsistencies before they affect the final payout.

By connecting each automation to a specific cost variable, insurers can explain the business case to finance without relying on a vague promise of “AI efficiency.”

Straight-Through Processing (STP) and Triage: Automating Low-Complexity Claims Safely

Straight-through processing allows an eligible claim to move from intake to settlement with little or no manual intervention.

It usually offers one of the fastest routes to ROI because low-severity, high-frequency claims often follow predictable rules. However, a successful STP strategy does not attempt to automate every claim. It identifies the claims that can safely follow a pre-approved pathway and routes everything else to the appropriate human team.

Four controls are particularly important:

- Eligibility rules covering active policies, applicable deductibles, satisfied conditions, and acceptable loss types

- Risk scoring for severity, fraud, litigation propensity, and anomalies

- Exception handling when a rule, threshold, or confidence requirement is breached

- Quality sampling to detect error, drift, unfair impact, or changing claim patterns

McKinsey notes that the technology for full straight-through processing of simple claims already exists and that AI-enabled systems can handle each step while allowing insurers to decide when human engagement is needed. Complex claims, however, still require human judgment, empathy, and expert review.

The practical rule is simple: automate triage first. Adjudication should only become touchless when coverage, severity, fraud risk, data quality, and confidence all support it.

Fraud and Anomaly Detection: Reducing Unnecessary Payouts Without Spiking False Positives

Insurance fraud creates direct financial loss, but poorly designed detection creates another problem: legitimate customers become trapped in unnecessary investigations.

The goal should not be to flag as many claims as possible. It should be to rank risk more accurately and help Special Investigation Unit teams focus on files with the strongest evidence.

Useful detection layers include attribute anomalies, network relationships, document forensics, and dynamic referral thresholds. A system may look for shared devices, repeated addresses, unusual repair-shop patterns, manipulated metadata, duplicated images, or claim combinations that rarely occur together.

Dynamic thresholds are especially important. Referral rules should reflect claim value, SIU capacity, and the insurer’s required balance between precision and recall. Sending every weak signal to investigators creates noise rather than value.

Fraud automation should place claims into appropriate handling tracks instead of reducing every case to a binary fraud-or-not-fraud label. Better ranking reduces unnecessary payouts while allowing low-risk claims to proceed faster.

High-Impact Use Cases Across the Claims Lifecycle (From FNOL to Settlement)

Claims automation works best when it follows the full lifecycle rather than isolated departmental boundaries. Poor intake affects triage. Weak document extraction affects fraud models. Incomplete estimates create supplements. Unclear status information generates calls.

A connected intelligent automation insurance strategy therefore begins at FNOL and expands gradually through document processing, triage, assessment, communication, and settlement.

FNOL and Intake Automation: Omnichannel Capture, Pre-Fill, and Eligibility Checks

The quality of FNOL data influences every step that follows. Missing or inconsistent information creates rework, delays, duplicate contact, and weak triage.

A strong intake workflow can capture information across web, mobile, email, voice, chat, and partner channels. It can pre-fill customer, asset, and policy information, verify coverage and deductibles, request missing evidence, and route the claim into an STP, fast-track, complex, or SIU pathway.

It can also trigger operational actions such as towing, glass repair, mitigation, or inspection scheduling.

When a claim is sent for manual review, the system should preserve the reason. These reason codes create the feedback loop required to improve triage rules, policy logic, and model performance over time.

Document Understanding (IDP): OCR + LLM Extraction for Emails, PDFs, and Images

Claims organizations process police reports, medical bills, invoices, proof-of-loss forms, repair estimates, receipts, emails, photos, and correspondence in inconsistent formats.

Intelligent Document Processing combines OCR, classification, extraction, validation, and confidence scoring to convert that material into usable structured data.

A governed IDP workflow should classify each document, extract relevant fields, retain the source location, validate values against the claim context, and route low-confidence results for human correction. Approved corrections should then feed evaluation and model improvement.

Microsoft Azure Document Intelligence combines deterministic extraction for structured documents with LLM-powered analysis for complex, unstructured, and multimodal content.

AWS describes IDP as a workflow that classifies, extracts, validates, integrates, and continuously improves document processing, including insurance claim verification. UiPath similarly positions IDP as a way for insurers to triage claims, improve service, and streamline billing and payment workflows.

The important lesson is that extraction accuracy alone is not enough. IDP creates value when validation, human correction, auditability, and downstream workflow are designed together.

Damage Assessment With Computer Vision (P&C): Faster Estimates, Fewer Supplements

Computer vision can shorten the path from customer-submitted photos to an initial damage assessment, particularly in auto and property claims.

A typical workflow includes guided photo capture, image-quality validation, damage identification, severity estimation, estimate assistance, and adjuster review.

The technology can check whether required views are present, identify visible damage, estimate likely complexity, suggest parts or labor, and detect patterns that commonly lead to supplements. Image-forensics checks can also help identify duplication or manipulation.

Guided photo capture is often as important as the vision model itself. Better inputs reduce inspection delays and improve estimate consistency.

The strongest deployment pattern is usually an AI-assisted estimate with adjuster oversight. This produces speed and consistency without placing an opaque model in control of a consequential settlement decision.

Customer Communication: AI Virtual Agents for Status Updates and Missing-Info Nudges

A large share of claims contacts involve routine questions: Where is my claim? What information is missing? When is my inspection? What happens next?

Virtual agents can reduce that volume when they are securely connected to the system of record and can complete small actions rather than merely answer FAQs.

Useful capabilities include authenticated status updates, reminders for missing information, appointment scheduling, and clear explanations of the next step. Sensitive conversations, negative sentiment, adverse decisions, and unusual cases should move quickly to a human.

LLMs should remain assistive in this use case. They can draft or simplify messages, but the underlying status, deadlines, and decisions should come from authoritative claim data and governed workflow rules.

Implementation Blueprint: How to Deploy Insurance Intelligent Automation Without Breaking Ops

Claims operations are production systems. An automation that introduces inconsistent outcomes, downtime, audit gaps, or new support burdens will quickly lose operational support.

The safest implementation begins with workflow economics, integration realities, risk tiers, and measurement. Model selection comes later.

Capgemini’s 2026 research, which was mentioned earlier, highlights a common problem: many insurers are capturing only marginal AI benefits, while 72% of spending goes to technology and only 28% to change management. Technology investment alone does not improve claims performance when operating models, KPIs, and adoption remain weak.

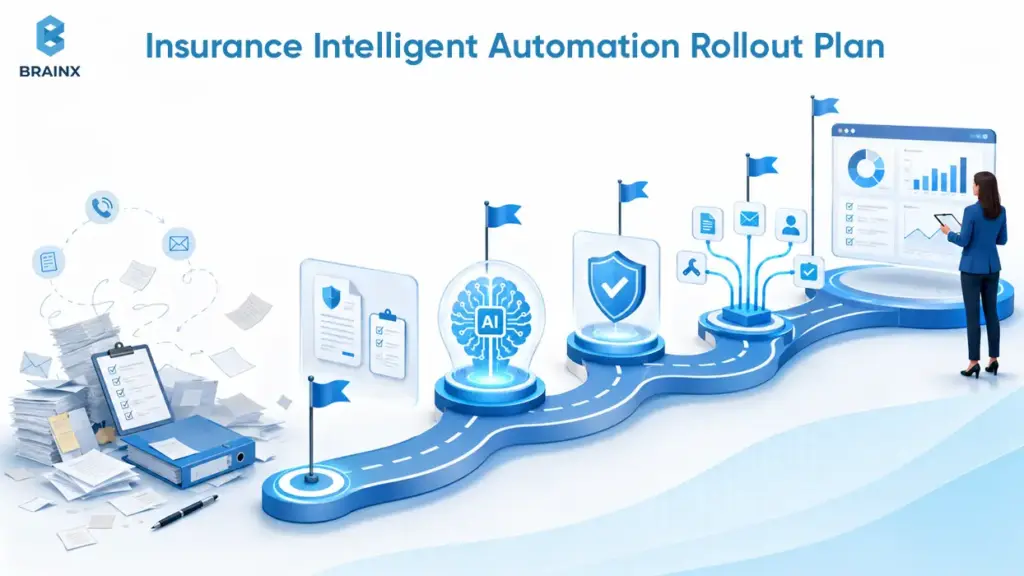

Insurance Intelligent Automation Rollout Plan

A dependable insurance intelligent automation rollout follows three phases.

Discover

Map the current journey and its exception paths. Quantify touches, queue time, rework, leakage, and contact volume. Assess data availability, permissions, lineage, and integration constraints. The main output should be a prioritized backlog showing expected value, feasibility, risk, controls, and measurement requirements.

Pilot

Select one to three high-volume, manageable use cases. Use a controlled production lane, shadow mode, or limited claim segment. Establish confidence thresholds, human fallback, monitoring, and comparison groups before launch.

A pilot around FNOL completeness, document extraction, or claims-status communication may fit into a 30-to-90-day window when the required data and integration paths are accessible.

Scale

Extend reusable components to adjacent claim types. Standardize logging, testing, approvals, and integration patterns. Introduce MLOps and LLMOps monitoring, assign operational ownership, and expand only after quality and financial gates have been met.

The goal is not the fastest possible deployment. It is a capability that can expand without creating new operational or technical debt.

Reference Architecture: Claims System + BPM/Workflow + RPA + AI Services + Data Layer

A durable architecture keeps the core claims system as the source of truth while adding a modular automation layer around it.

The main layers include:

- Systems of record: Claims, policy administration, billing, customer, and payment platforms

- Workflow/BPM: Tasks, queues, SLAs, approvals, timers, and exception handling

- Integration layer: APIs, events, connectors, middleware, and ETL where necessary

- AI services: IDP, triage scoring, fraud detection, computer vision, retrieval, and summarization

- Selective RPA: Stable legacy tasks where reliable APIs are unavailable

- Data layer: Analytics warehouse, feature store, document repository, and vector database

- Observability: Accuracy, drift, latency, cost, overrides, failures, and business outcomes

The most important design principle is separation of concerns. Business-critical rules should not be buried inside opaque prompts. Coverage logic, adverse-decision criteria, thresholds, and approvals should remain explicit, versioned, and testable.

RPA should bridge stable legacy gaps. It should not become the backbone of the claims architecture.

Human-in-the-Loop and Audit Trails: Designing Controls for Regulated Decisions

NAIC guidance states that insurers remain responsible for legal compliance, fairness, accuracy, and avoiding unfair discrimination when AI supports insurance decisions. It also emphasizes the continuing importance of human oversight.

NIST’s AI Risk Management Framework is intended to help organizations incorporate trustworthiness considerations into the design, development, use, and evaluation of AI systems.

Claims workflows should therefore include confidence-based routing, human approval for high-impact outcomes, and decision logs containing source data, model versions, evidence, reason codes, and overrides.

High-severity settlements, denials, suspicious claims, or ambiguous policy interpretations may require a four-eyes review. LLM-supported recommendations should link back to the relevant policy or procedure, and samples of touchless claims should be reviewed regularly for drift or systematic error.

Human review is not a sign that the automation failed. It is a deliberate control that allows the insurer to automate routine work without losing accountability.

Integration Realities: Legacy Cores, Vendor APIs, Data Quality, and Change Management

Most programs struggle more with integration and adoption than with the AI model itself.

Claims cores may be heavily customized. Vendor APIs may behave differently across products. Documents may lack consistent labels. Historical outcomes may contain incomplete reason codes. Frontline teams may distrust outputs they cannot inspect.

To reduce these risks, insurers should favor event-driven triggers, build a stable internal API layer around core-system quirks, and treat data quality as an owned operational product.

Shadow-mode testing can show how the automation would behave before it affects live outcomes. SOPs, approval rules, exception procedures, and team responsibilities should also be updated before launch.

Change management begins during discovery, not after deployment. When supervisors see fewer reopenings, shorter queues, and fewer status calls, adoption becomes easier.

Build vs Buy (and What to Outsource): Making the Right Product & Platform Choices

The right decision is not simply whether to build or buy AI. It is which capabilities are commodity, which are differentiating, and which will become expensive or brittle if the insurer owns them directly.

A practical rule is to buy the undifferentiated plumbing, customize the decision flow, and keep claims metrics and governance under internal control.

Choosing the Automation Approach: Point Tools vs Platforms vs Custom AI Workflows

| Approach | Best Fit | Main Limitation |

| Point tools | Narrow requirements such as OCR, e-signature, transcription, or image-quality checks | Integration sprawl when too many tools are deployed |

| Platforms | Reusable workflow, orchestration, governance, monitoring, and multiple claims use cases | Vendor lock-in and slower customization |

| Custom AI workflows | Proprietary rules, unusual integrations, complex exceptions, and differentiated decision logic | Higher initial engineering and ownership requirements |

Most insurers will benefit from a hybrid model: use a platform for workflow and observability, proven specialist tools for IDP or vision, and custom logic for triage, policy-aware decisioning, integration, and governance.

This provides speed without surrendering control over claims economics, customer experience, or regulatory accountability.

Vendor Evaluation Checklist: Security, SOC2, Data Residency, Model Transparency, TCO

A polished demo does not prove that a solution can operate safely inside a claims environment.

A serious evaluation should cover:

- Security certifications, encryption, access control, and tenant isolation

- Data residency, subprocessors, retention, and deletion policies

- Confidence scores, model versions, explainability, and change logs

- Audit trails for extracted fields, recommendations, overrides, and LLM outputs

- API maturity, event support, connectors, sandboxes, and rate limits

- Per-document, per-claim, per-token, implementation, and support costs

- SLAs, incident response, rollback, retraining, and disaster recovery

Total cost of ownership extends beyond licensing. Models require evaluation, connectors require maintenance, workflows change, and core-system upgrades can break poorly designed integrations.

KPI Dashboard: How to Measure Success in Claims Automation

If finance cannot see the economic difference, the program will remain an interesting experiment.

Every intelligent automation insurance initiative should have a dashboard before it has a production launch date. Establish a baseline for 60 to 90 days, then compare controlled cohorts by line of business, complexity tier, region, and handling route.

Illustrative sample data. Actual baselines and targets should be segmented by claim type, region, complexity, and handling path.

Core KPIs: Cycle Time, Touchless Rate, Reopen Rate, Leakage, SIU Referral Precision

A balanced KPI set should include:

- Median and p90 time to contact, decision, and settlement

- Touchless or touch-light rate

- Reopen and supplement rates

- Leakage and indemnity variance

- Adjuster caseload, handling time, and queue aging

- Customer contacts, complaints, NPS, and CSAT

- SIU referral precision

- Human override rate and override reasons

Segmentation is essential. If the touchless rate improves while reopenings, supplements, or complaints also rise, the program is probably automating the wrong claim segment.

Proving Savings to Finance: Attribution, A/B Testing, and Cohort-Based ROI

Do not compare the entire claims book before and after implementation. Changes in catastrophe mix, geography, severity, and claim type can make that comparison misleading.

Instead, connect each automation to a specific cost bucket and compare similar claims handled through automated and manual routes. Where appropriate, use controlled routing or holdout groups.

Measure unit economics such as cost per claim, contact, document, and successful automated action. Quality gates should prevent expansion if reopenings, complaints, false positives, or indemnity variance exceed agreed limits.

The final test is benefit persistence. A saving that disappears after the initial implementation period is not a durable operating improvement.

Risks, Pitfalls, and What Breaks Most Claims Automation Programs

Claims automation usually fails because of workflow, data, governance, or adoption problems, not because AI is universally incapable.

The most dangerous assumption is that an intelligent automation insurance platform can fix a process the organization has not clearly defined.

Common Mistakes: Automating Broken Processes, Ignoring Exceptions, and Weak Governance

Common failure modes include:

- Automating an inefficient or inconsistent process

- Forcing exceptions through touchless pathways

- Leaving data quality without a clear owner

- Deploying without a feedback loop from adjuster corrections

- Failing to separate recommendations from regulated final decisions

- Measuring activity instead of financial and customer outcomes

- Treating governance as documentation rather than monitoring

- Scaling before frontline teams trust the workflow

A useful test is simple: if a regulator, auditor, customer, or plaintiff’s attorney questioned a decision, could the insurer retrieve the source data, model version, evidence, reason codes, and human approvals within minutes?

GenAI Guardrails in Claims: Prompt Patterns, Retrieval, Evaluation, and Escalation Rules

LLMs can help with claim summaries, correspondence drafts, document questions, knowledge retrieval, and missing-information detection. Claims operations, however, are not an appropriate environment for unrestricted generation.

Practical guardrails include retrieval over approved policies and procedures, structured outputs, instructions not to guess, and escalation when information is missing or confidence is low.

Teams should also maintain an evaluation set covering normal, edge, and adversarial claims. Red teaming should test prompt injection, data leakage, unsafe recommendations, and manipulated source material.

NIST’s Generative AI Profile identifies confabulation, privacy, harmful bias, automation bias, and information-integrity risks. It also recommends documented oversight, regular risk measurement, evaluation, red teaming, and continuous monitoring across the AI lifecycle.

The safest pattern is to let LLMs assist with interpretation and drafting while deterministic systems remain responsible for policy rules, workflow state, approvals, and payment execution.

How BrainX Helps With Intelligent Automation in Insurance

Insurers rarely need “more AI” in isolation. They need a governed claims automation program that integrates with existing systems, produces measurable outcomes, and can scale without weakening control.

BrainX Technologies supports intelligent automation insurance initiatives through five connected stages:

- Discovery and workflow mapping: Identify high-volume bottlenecks, exception paths, data dependencies, and realistic automation candidates.

- Pilot implementation: Build a controlled use case around FNOL, IDP, fraud scoring, computer vision, customer communication, or another measurable claims workflow.

- Integration and production controls: Connect the solution to legacy or cloud claims systems and implement APIs, audit trails, monitoring, human approval, and exception routing.

- MLOps and LLMOps: Support models and LLM workflows with versioning, evaluation, drift monitoring, and controlled updates.

- Scaling and governance: Extend reusable architecture and control patterns to additional claim types, products, regions, and teams.

BrainX’s Copyright Clinic case study also demonstrates its ability to automate intake and workflow activities in a regulated service environment. The solution combined AI-assisted pre-screening, scheduling, payments, dashboards, and notifications, reportedly reducing intake time significantly.

Talk to the BrainX AI team about identifying your highest-value claims workflow and building a governed pilot around measurable KPIs.

Conclusion

Meaningful claims savings do not come from a single platform purchase. They come from a staged operating model upgrade.

Start with intake and triage. Add document understanding, fraud and anomaly signals, and proactive customer communication. Expand touchless adjudication only where data quality, confidence, policy rules, and controls justify it.

When intelligent automation insurance is supported by human oversight, strong integration, and finance-grade measurement, it can reduce costs while improving consistency and customer experience.

Measure early, govern tightly, and scale thoughtfully. Treat claims automation as a capability that improves each quarter, not a one-time implementation.

FAQs About Intelligent Automation in the Insurance Industry

What Is Intelligent Automation for Insurance and How Is It Different From RPA?

RPA automates deterministic tasks such as copying data between systems or triggering standard actions. Intelligent automation insurance adds document understanding, machine learning, computer vision, LLM-assisted retrieval, and workflow orchestration.

It can interpret unstructured inputs, support routing, and recommend next steps based on confidence and risk. RPA remains useful as a tactical bridge when reliable APIs are unavailable, but it should not control the complete claims journey.

Can Intelligent Automation in Insurance Significantly Reduce Claims Costs?

Yes. Intelligent automation can materially reduce claims costs, but there is no universal percentage.

It can reduce handling expenses, rework, leakage, customer-contact volume, and unnecessary investigations. The size of the savings depends on the line of business, existing process maturity, data quality, integration complexity, and the share of claims that can safely move through touchless or touch-light workflows.

A controlled pilot with clear baselines and quality gates is the safest way to establish a realistic target.

Which Claims Processes Should Be Automated First for Fastest ROI?

The best starting points are usually FNOL completeness, coverage checks, low-complexity triage, document extraction, and proactive status communication.

These processes affect high claim volumes, create significant downstream rework, and are relatively easy to measure. Fraud scoring can also provide early value when the insurer has labeled outcomes and sufficient SIU capacity.

Complex adjudication and negotiation should come later, once controls and monitoring have been proven.

What Data Do Insurers Need to Implement AI for Claims Automation?

Insurers typically need historical claims and outcomes, policy limits and exclusions, FNOL information, workflow timestamps, exception codes, documents, communications, and stable identifiers connecting customers, policies, claims, and evidence.

Repair, provider, fraud, image, and third-party data may also be needed for more advanced use cases.

The data does not have to be perfect, but it must be accessible, permissioned, traceable, and governed.

How Do You Keep Humans in the Loop and Stay Compliant With AI-Driven Claims Decisions?

Use confidence thresholds and decision-risk tiers to determine which claims require human review.

Record model versions, source data, prompts, reason codes, overrides, and approvals. Require source-linked outputs for policy interpretations and stronger review for high-severity, adverse, or suspicious outcomes.

Ongoing sampling, drift monitoring, bias evaluation, and documented change approvals help ensure the system remains accurate and defensible after deployment.

How Long Does It Take to Implement Insurance Intelligent Automation in a Claims Department?

A focused pilot can often be delivered in 6 to 12 weeks when the workflow is well-defined and the required data and integrations are accessible.

Scaling across lines of business usually takes several quarters because production deployment also requires security reviews, exception design, monitoring, training, governance, and change management.

The most reliable approach is phased: prove value in one claim lane, harden the controls, and expand using reusable architecture and workflow patterns.